The weather in the main producing areas has always been one of the important factors affecting the oil plate. Since the end of May, under the influence of the increasing demand in the main selling countries and the slow increase in production in the producing areas, the accumulation of palm oil in the producing areas was less than expected, which boosted the domestic palm oil performance. However, the precipitation in the main soybean and rapeseed producing areas in North America has been abundant, and the weather transaction has been delayed, which makes the performance of domestic soybean oil and vegetable oil weak. At present, the contract price difference between bean brown and vegetable brown 2409 is at the lowest level in the past five years, with the difference of 540 yuan/ton and 831 yuan/ton from the second lowest level in the same period, which also has the need for upward repair. However, it is still necessary to be vigilant that the crop situation in North America continues to be good, which makes the prices of soybean oil and vegetable oil lack the possibility of upward drive.

The spread between bean brown and vegetable brown is expected to widen again in the third quarter.

Tony

Palm oil: tight supply pattern may improve

Since the end of May, under the influence of the increasing demand in the main selling countries and the slow increase in production in the producing areas, the accumulation of palm oil in the producing areas was less than expected, which boosted the domestic palm oil performance. However, the precipitation in the main soybean and rapeseed producing areas in North America has been abundant, and the weather transaction has been delayed, which makes the performance of domestic soybean oil and vegetable oil weak. After the transformation of the relationship between oil strength and oil strength, the spread between bean brown and vegetable brown, which had been greatly expanded in the previous period, shrank again. As of the close of July 8th, the contract spreads of bean brown and vegetable brown 2409 closed at -12 yuan/ton and 820 yuan/ton respectively. However, the tight supply of palm oil at home and abroad has improved marginally, and soybean oil and vegetable oil may be traded in North America. Therefore, the price difference between soybean palm and vegetable palm is expected to widen again in the third quarter.

With regard to palm oil, we believe that after entering the third quarter, with the continuous growth of production in the producing areas and the peak of domestic arrivals, the tight supply pattern of palm oil at home and abroad will be eased, and the support for prices will be weakened.

On the supply side of producing area, the traditional growth period of Malaysian palm oil is from March to October every year, and the growth rate of palm oil from June to October is faster than that from March to May. Palm oil production in Malaysia has recovered well this year: from January to May, palm oil production totaled 7.26 million tons, up 9.44% year-on-year, which boosted the market’s confidence in its performance in the subsequent production increase season. Last year, the El Ni? o phenomenon had little impact on Malaysia, and only a few months had obvious drought. This year, the country’s output is not expected to be seriously affected, so the subsequent increase in palm oil production in Malaysia from July to October can still be expected. According to the data of the Southern Peninsula Palm Oil Crusher Association (SPPOMA), from July 1 to 5, the palm oil yield in Malaysia increased by 59.39%, the oil yield decreased by 0.12%, and the output increased by 58.36%.

The uncertainty of palm oil supply in the future is mainly in Indonesia. During the El Ni? o phenomenon last year, the precipitation in the country was seriously lacking, and the delay effect began to appear in the second quarter of this year. In the follow-up, there was the possibility that the output increased less than expected or even decreased year-on-year.

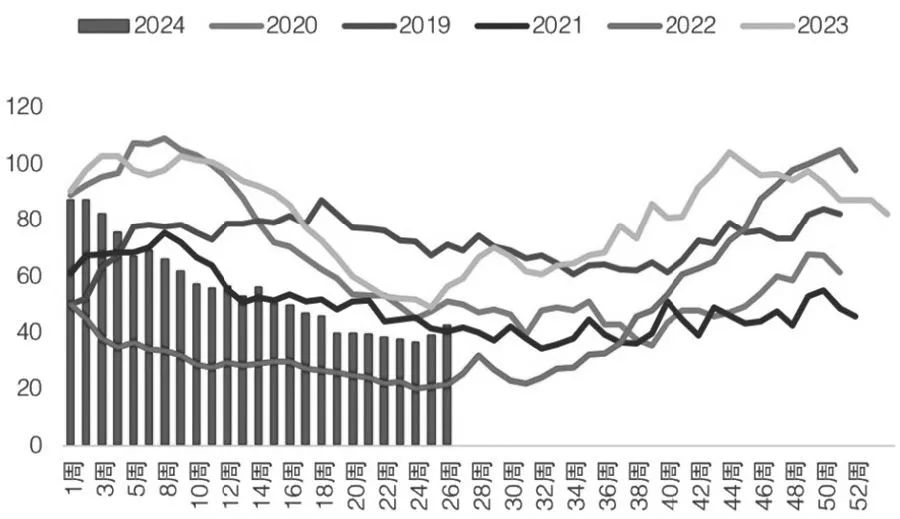

On the demand side of producing area, although palm oil stocks in major selling countries such as India and China are low, there will be import demand for replenishment in the future. However, Argentina has set a high soybean yield in 2023/2024, which will flow into the international market in large quantities after being crushed in the factory, crowding out India’s palm oil import demand. Due to the continuous growth of supply and the uncertainty of demand, we believe that the general trend of palm oil inventory in the producing area will remain unchanged in the third quarter, mainly because the accumulation rate will slow down and the supply and demand tension will decrease marginally.

There is a similar situation in the supply and demand of palm oil in China. From June to September, the amount of palm oil arriving in Hong Kong is expected to be 330,000 tons, 380,000 tons, 360,000 tons and 430,000 tons, which is a significant increase compared with the monthly average of less than 200,000 tons from January to May. Although summer is the traditional peak season for palm oil consumption, it is expected that the downstream consumption will also increase after the temperature rises. However, under the impact of huge arrivals, the general trend of palm oil accumulation in China will remain unchanged, but the speed will slow down. The strong position of palm oil will be weakened in the future under the decreasing marginal tension of production area and domestic supply and demand.

The picture shows the domestic palm oil inventory (unit: 10,000 tons)

Soybean oil and vegetable oil: paying attention to the influence of extreme weather

In terms of soybean oil and vegetable oil, the environment and growth of American soybean and Canadian rapeseed in 2024/2025 are good.

In terms of American beans, the latest excellent and good rate as of July 7 was 68%, higher than 51% in the same period last year and 67% predicted by the market. The proportion of areas affected by drought in the main producing areas of American soybeans rose to 9%, but it was still far lower than 60% in the same period last year. In terms of Canadian rapeseed, as of the week of July 2, the latest excellent rate in Alberta was 66.8%, much higher than 42.90% in the same period last year; 75.3% of the regional soil moisture in this province is in the good to good range, which is higher than the five-year average of 61.5% and the ten-year average of 61.6%. The good growth of crops in the two countries has suppressed the domestic soybean oil and vegetable oil prices, which is one of the important reasons for the continuous decline in the price difference between soybean brown and vegetable brown in the early stage.

However, after entering the third quarter, with the new crop in North America gradually entering the critical growth period, the impact of extreme weather such as La Nina phenomenon and global warming will become more and more prominent this year, and subsequent weather transactions are expected to bring opportunities for soybean oil and vegetable oil to strengthen in stages. The short-term weather forecast shows that in the next 1-2 weeks, the main producing areas of soybean and rapeseed will be covered by high temperature, and the precipitation in the main producing areas of rapeseed will be less. The long-term weather forecast from July to September is even more pessimistic, which shows that there are high-temperature disasters in the United States and Canada during this period, and there are large precipitation-missing areas in Alberta, Saskatchewan and northern Manitoba, Canada, which are not conducive to the growth and development of crops that have entered the flowering and pod-setting stage.

In order to further analyze the impact of extreme weather on crops in North America this year, we counted the changes in the yield of American beans and Canadian rapeseed during La Nina phenomenon. Statistics show that there have been four La Nina phenomena covering the growing season of American beans and Canadian rapeseed since 2000, which has affected the crop growth for seven years. Among them, the yield of American soybean and rapeseed decreased by 54% year-on-year, with a decrease rate of 1.14%~4.06% (American soybean) and 0.43%~32.05% (Canadian rapeseed). It can be seen that under the La Ni? a phenomenon environment, the yield reduction probability of the two crops has improved to some extent.

In addition, the recent resurgence of rapeseed frost news in Europe is also expected to further tighten the rapeseed supply in 2024/2025, which was tightened year-on-year, and support the domestic vegetable oil price. The latest local survey shows that the rapeseed in the EU in 2024/2025 was seriously affected by the frost at the end of April. With the subsequent harvest to verify the yield reduction, there is a possibility that the yield will be lowered beyond expectations. And consulting organizations such as Council of Europe and Oil World also lowered the EU rapeseed production in 2024/2025, further aggravating the atmosphere of doing more. The further tightening of rapeseed supply in the EU has also boosted the international vegetable oil price and transmitted it to China.

There is an upward repair demand for the spread between bean brown and vegetable brown.

To sum up, on the one hand, the production area and domestic palm oil will continue to accumulate in the third quarter of this year, and the tight supply and demand trend in the second quarter will decrease marginally, weakening the price support. On the other hand, the probability of weather trading increases after North American crops enter the critical growth period, and the unexpected reduction of rapeseed production in the European Union may further tighten the global rapeseed supply and demand, which will help soybean oil and vegetable oil to get out of the staged strong market and drive the spread between soybean brown and vegetable brown.

At present, the contract price difference between bean brown and vegetable brown 2409 is at the lowest level in the past five years, which is 568 yuan/ton and 987 yuan/ton lower than the second lowest level in the same period, and it also has the need for upward repair. However, it is still necessary to be vigilant that the crop situation in North America continues to be good, which makes the prices of soybean oil and vegetable oil lack the possibility of upward drive. In operation, it is suggested that the spread between bean brown and vegetable brown 2409 should be expanded on dips. (Author: Changjiang Futures)

The above contents are for reference only, so you should enter the market at your own risk.

Analyst: It is difficult for vegetable oil to have a big independent trend in the second half of the year.

Zheng quan

Recently, the sentiment of the oil and fat market has continued to weaken, and the disk has collectively declined. Among them, vegetable oil closed down by 1.88%, and rapeseed meal plunged by 3.3%. So, how will vegetable oil be interpreted in the second half of the year?

"In the report released on June 24, the EU Crop Monitoring Service (MARS) continued to reduce the EU rapeseed yield by 0.05 tons/hectare, corresponding to a reduction of about 300,000 tons. EU rapeseed was harvested from mid-to-late June to August, and the reduction in production has become a reality. " Liu Ruijie, an oil and fat analyst at Shandong Qisheng Futures, told the Futures Daily that Ukrainian rapeseed exports were exhausted in 2023/2024, and the exportable supply to the EU in July was very low, which will continue to support the price of vegetable oil in the EU. In 2024/2025, EU rapeseed production decreased, and Ukraine rapeseed production decreased. At present, both of them are in the early stage of harvest. With the advance of harvest, EU rapeseed supply will increase in August. However, in view of the bright prospect of rapeseed production reduction in 2024/2025, the pressure will be lighter than in previous years, even in the harvest market period. Therefore, only Canada rapeseed is the main consumer and exporter in the world, and Canada rapeseed will be the only window to increase exports.

Tao Zhaohui, an oil and fat analyst, said that from the current situation, the overall supply of world oil in 2024/2025 is expected to be sufficient. The weather of rapeseed in American soybean producing areas and Canada is generally good. Although the strategic grain company slightly lowered the EU rapeseed production a little earlier, the downward adjustment was limited, and the expected decline in the world rapeseed production was limited.

According to Jia Hui, an oil and fat analyst at Zhonghui Futures, the overall supply pressure of domestic vegetable oil in the first half of the year was not great, and after the domestic sunflower oil price rose in the second quarter, it was conducive to the increase of vegetable oil consumption demand, and the upward pressure on prices was also alleviated. Because the rapeseed crushing capacity of coastal oil plants in the first half of the year was lower than that of the same period last year, the supply of rapeseed oil crushing decreased. The data shows that as of June 28th, the pressed amount of rapeseed was 2.272 million tons, which was lower than 2.9375 million tons in the same period last year.

On the import side, from January to May, China imported 807,500 tons of low erucic rapeseed oil, which was lower than 963,700 tons in the same period last year. As of June 28th, Mysteel statistics show that the vegetable oil inventory of coastal oil plants is 101,500 tons, which is lower than that of 110,500 tons in the same period last year, but the inventory data is still significantly higher than that of the same period in 2021 and 2022. Jia Hui said that from the perspective of crushing imports and inventory, the domestic supply pressure this year is relatively small.

"In fact, China’s vegetable oil import in 2024/2025 is expected to drop to 1.7 million tons, down 450,000 tons from 2.15 million tons in 2023/2024, while the rapeseed import is also expected to drop slightly to 3.2 million tons (3.4 million tons in 2023/2024), and the ending inventory of vegetable oil will be reduced from 1.588 million tons in 2023/2024. The declining inventory will bring some support to the vegetable oil. " Tao Chaohui said.

In addition, the related oils and fats are also mixed. Tao Zhaohui said: First, soybean oil, because the world soybean supply is expected to increase to 422.26 million tons in 2024/2025, and the ending inventory is expected to increase to 127.9 million tons, coupled with the growth of soybean imports in China, the soybean oil inventory of oil plants is at the second highest level in five years, which is unfavorable for the upward price; Second, palm oil, mainly due to the long-term support of biodiesel policy and a slight decline in the inventory at the end of the world, is relatively strong, or brings corresponding support to vegetable oil.

Looking forward to the market outlook, Liu Ruijie thinks that, considering the global rapeseed supply and demand, the export of Canadian rapeseed in 2023/2024 and 2024/2025 is likely to be increased, and it is estimated that the stock-to-sales ratio of Canadian rapeseed in 2024/2025 may drop below 8%. In the fourth quarter and the second quarter of next year, faced with the competition of import demand from other countries, the import and supply of rapeseed has great variables. It is estimated that domestic vegetable oil will start to go to the warehouse in August, and unilaterally focus on the cost-side logic and the subsequent transmission of supply and demand logic.

"Looking forward to the market in the second half of the year, from the data of the June report released by USDA, the global rapeseed production and ending inventory in 2024/2025 decreased year-on-year, and the annual supply performance tightened. However, due to the global climate change, from the current and future weather outlook, rapeseed planting in Canada and Australia is expected to be smooth. Judging from the short-term and medium-term weather forecast, the weather in Canada’s rapeseed producing areas is normal, which is conducive to rapeseed growth. From June to August, only a small number of rapeseed producing areas in Australia are dry, but at present, the impact will not be great. If the international rapeseed planting lacks the theme of weather premium trading, it is expected that the price of vegetable oil in the third quarter will be difficult to have a more obvious trend to see more markets. " Jia Hui said that domestically, due to the decline in rapeseed crushing in the second half of the year, coupled with the stocking demand of "Golden September and Silver 10" and the consumption demand after the weather turns cold, the price center of gravity is expected to move up gradually in the shock, but the overall market is mainly based on soybean oil and palm oil. If the weather is good and there are no major changes in national and industrial policies, it is expected that vegetable oil will not have a large independent trend.